“`html

Most people dream of earning more money. They believe a higher salary, better business income, or additional side hustles will automatically solve their financial problems. However, millions of people earn more today than they did a few years ago and still struggle to build lasting wealth.

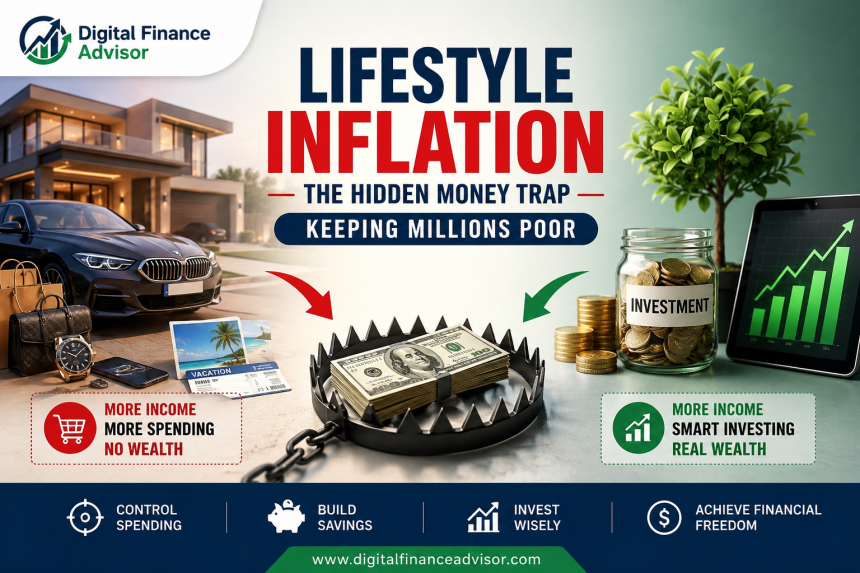

The reason is often Lifestyle Inflation.

Lifestyle Inflation is one of the most common yet overlooked financial traps. It occurs when spending rises alongside income. Instead of using raises, bonuses, or business profits to increase savings and investments, many people upgrade their lifestyles. They move into larger homes, buy newer vehicles, dine at expensive restaurants, take luxury vacations, and subscribe to premium services.

While there is nothing wrong with enjoying the rewards of hard work, uncontrolled Lifestyle Inflation can quietly destroy your wealth-building potential. Over time, increased expenses absorb every extra dollar earned, leaving little room for saving, investing, or achieving financial freedom.

If you want to build long-term wealth, understanding Lifestyle Inflation is essential. This comprehensive guide explains how Lifestyle Inflation works, why it happens, the hidden dangers it creates, and proven strategies to avoid it.

What Is Lifestyle Inflation?

Lifestyle Inflation refers to the tendency for spending to increase as income increases.

When people earn more money, they often improve their standard of living by spending more on housing, transportation, entertainment, technology, and everyday conveniences.

For example:

- You receive a salary increase and move into a larger apartment.

- You get promoted and purchase a luxury vehicle.

- Your business becomes more profitable and you increase discretionary spending.

- You start earning more and subscribe to multiple premium services.

Individually, these upgrades may seem harmless. However, when they become a recurring pattern, they can prevent meaningful wealth accumulation.

This phenomenon is also known as lifestyle creep.

Why Lifestyle Inflation Happens

Understanding the causes of Lifestyle Inflation can help you avoid falling into the trap.

1. Social Comparison

Humans naturally compare themselves to others. Friends buying new cars, coworkers upgrading homes, and influencers displaying luxury lifestyles on social media can create pressure to spend more.

Many purchases are motivated not by necessity but by the desire to keep up with perceived social expectations.

2. Rewarding Success

Many people view spending as a reward for their achievements.

Examples include:

- Promotion = New Car

- Bonus = Luxury Vacation

- Business Growth = Expensive Lifestyle Upgrade

Although rewarding yourself occasionally is healthy, repeatedly converting income gains into lifestyle upgrades can limit long-term financial growth.

3. Easy Access to Credit

Modern financial systems make spending easier than ever.

Credit cards, financing offers, personal loans, and buy-now-pay-later services allow consumers to purchase expensive items without feeling the full financial impact immediately.

This encourages Lifestyle Inflation even when cash flow is limited.

4. Hedonic Adaptation

Psychologists refer to a concept called hedonic adaptation, which means people quickly become accustomed to improved circumstances.

A new luxury vehicle feels exciting initially, but after a few months it becomes normal. Soon another upgrade feels necessary.

This cycle can continue indefinitely.

Common Examples of Lifestyle Inflation

Lifestyle Inflation often appears gradually through everyday spending decisions.

Housing Upgrades

- Larger homes

- Luxury apartments

- Expensive renovations

- Premium furniture purchases

Transportation Upgrades

- Luxury vehicles

- Frequent vehicle replacements

- Higher insurance costs

- Premium vehicle maintenance

Dining and Entertainment

- Frequent restaurant visits

- Food delivery services

- Premium streaming subscriptions

- Expensive hobbies

Technology Spending

- Annual smartphone upgrades

- High-end electronics

- Smart home devices

- Premium software subscriptions

Travel and Leisure

- Luxury vacations

- Business-class flights

- Premium hotel accommodations

- High-end recreational activities

The Hidden Cost of Lifestyle Inflation

The real danger of Lifestyle Inflation is not the money spent today.

The real danger is the future wealth that money could have created.

Consider the following example:

- Annual Salary Increase: $10,000

- Additional Annual Spending: $8,000

- Additional Savings: Only $2,000

At first glance, spending an extra $8,000 may not seem significant. However, if that money were invested consistently over decades, it could grow into hundreds of thousands of dollars.

This is where opportunity cost becomes extremely important.

The Power of Compound Growth

Compound growth is one of the most powerful forces in personal finance.

Let’s assume you invest $500 monthly instead of spending it on lifestyle upgrades.

- 10 Years at 8% Annual Return = Approximately $91,000

- 20 Years at 8% Annual Return = Approximately $294,000

- 30 Years at 8% Annual Return = Approximately $745,000

Small spending decisions made today can significantly impact your financial future.

This is why controlling Lifestyle Inflation is critical for wealth building.

How Lifestyle Inflation Prevents Wealth Building

Successful wealth building depends on one simple principle:

Spend less than you earn and invest the difference.

Two individuals earning identical salaries can have dramatically different financial outcomes based on spending habits.

Example:

Person A:

- Saves and invests 30% of income.

- Controls Lifestyle Inflation.

- Maintains moderate living expenses.

Person B:

- Spends nearly every raise.

- Regularly upgrades lifestyle.

- Maintains high monthly expenses.

After twenty years, Person A will likely have a substantially larger net worth despite earning the same income.

Income creates opportunity. Spending determines outcomes.

Warning Signs of Lifestyle Creep

You may be experiencing Lifestyle Inflation if:

- Your expenses rise every time your income increases.

- You struggle to save despite earning more than before.

- Your savings rate remains stagnant.

- You frequently upgrade electronics and vehicles.

- You justify purchases based on monthly payments.

- You earn more but do not feel financially secure.

- Your credit card balances continue growing.

Recognizing these signs early can help prevent long-term financial damage.

How Lifestyle Inflation Delays Financial Freedom

Financial freedom means having enough assets and investments to support your desired lifestyle without relying solely on active employment.

Lifestyle Inflation makes achieving this goal much harder.

For example:

- Annual Expenses = $30,000

- Required Investment Portfolio = Much Smaller

- Annual Expenses = $80,000

- Required Investment Portfolio = Significantly Larger

The more expensive your lifestyle becomes, the more wealth you must accumulate to sustain it.

Reducing unnecessary expenses can dramatically accelerate your journey toward financial freedom.

7 Proven Strategies to Avoid Lifestyle Inflation

1. Automate Savings and Investments

Automatically transfer money into investment accounts before you have the opportunity to spend it.

Automation removes emotion from financial decision-making.

2. Follow the 50% Rule for Raises

Whenever your income increases:

- 50% goes to investments.

- 30% goes toward financial goals.

- 20% can be used for lifestyle improvements.

This allows you to enjoy increased income while continuing to build wealth.

3. Maintain a Budget

Effective budgeting allows you to monitor spending and identify areas where Lifestyle Inflation may be occurring.

Track categories such as:

- Housing

- Transportation

- Food

- Entertainment

- Subscriptions

- Savings

- Investments

4. Delay Major Purchases

Implement a 30-day waiting period before making large purchases.

This reduces emotional spending and improves financial decision-making.

5. Focus on Net Worth Instead of Income

Many people celebrate income increases while ignoring net worth growth.

True financial success is measured by assets, investments, and overall wealth accumulation.

6. Avoid Status Purchases

Before buying expensive items, ask yourself:

Am I purchasing this because it improves my life or because it impresses other people?

7. Review Your Finances Monthly

Regular financial reviews help identify spending patterns and prevent Lifestyle Inflation from becoming permanent.

The Importance of Strong Money Habits

Developing strong money habits is one of the best defenses against Lifestyle Inflation.

Effective money habits include:

- Tracking expenses

- Following a budget

- Investing consistently

- Avoiding impulse purchases

- Setting financial goals

- Maintaining an emergency fund

Over time, these habits compound into significant financial advantages.

Real-Life Example of Lifestyle Inflation

Imagine two professionals who each receive a $20,000 annual raise.

Professional A:

- Purchases a luxury vehicle.

- Moves into a larger home.

- Increases dining and entertainment spending.

- Saves very little.

Professional B:

- Maintains existing lifestyle.

- Invests most of the raise.

- Builds an emergency fund.

- Increases retirement contributions.

After ten years, Professional B will likely possess a substantially higher net worth despite earning the same income.

The difference lies in financial behavior, not earnings.

Frequently Asked Questions About Lifestyle Inflation

What is Lifestyle Inflation?

Lifestyle Inflation occurs when spending increases as income rises, reducing the amount available for saving and investing.

Is Lifestyle Inflation always bad?

No. Moderate lifestyle improvements can improve quality of life. Problems arise when spending consumes most or all income growth.

What is lifestyle creep?

Lifestyle creep is another term for Lifestyle Inflation and refers to the gradual increase in spending over time.

How can I avoid Lifestyle Inflation?

Create a budget, automate investments, control discretionary spending, and prioritize long-term financial goals.

Can high-income earners suffer from Lifestyle Inflation?

Yes. Many high-income professionals struggle financially because their spending increases alongside their income.

Final Thoughts

Lifestyle Inflation is one of the biggest hidden barriers to wealth building and financial freedom.

While earning more money creates opportunities, increasing spending at the same pace can prevent meaningful financial progress.

The most successful wealth builders understand a simple principle:

It is not how much money you make that determines your wealth. It is how much money you keep and invest.

By controlling Lifestyle Inflation, developing strong money habits, maintaining a budget, and consistently investing, you can build long-term wealth and achieve true financial freedom.

Remember: Wealth is often built quietly through disciplined financial decisions, not visible displays of success.

“`